In the Oil & Gas industry, multi-million-dollar drilling rigs and complex completion designs often steal the headlines. But the long-term profitability of any well is determined not just by how much it produces, but by how efficiently it operates day after day. This is where Lease Operating Expense (LOE) comes in.

LOE is one of the largest and most complex ongoing costs for any producer. Without a disciplined approach to budgeting and management, rising operating costs can quietly cripple the economics of a well, turning a promising asset into a financial drain.

This guide will provide a deep dive into the world of LOE, offering a practical framework for operations managers and financial analysts to effectively budget, forecast, and control these critical costs to maximize the value and lifespan of every asset in your portfolio.

Before you can build a budget, you must clearly define its scope. Lease Operating Expense encompasses all the daily, direct costs incurred to keep a well producing oil and gas after the initial drilling and completion phases are finished. In simple terms, it's the cost of "keeping the lights on" at the well site.

It's just as important to understand what LOE is not. It does not include the upfront Capital Expenditure (CapEx) to drill and complete the well, nor does it include exploration costs, corporate overhead (G&A), interest, or production taxes. It is purely the direct operational cost at the lease level.

The primary components of LOE can be broken down as follows:

| Category | Description | Common Examples |

|---|---|---|

| Labor | Costs for field personnel operating the wells. | Contract pumper fees, field supervisor salaries, roustabout services. |

| Equipment & Maintenance | Costs to keep surface and downhole equipment running. | Pumpjack rental, routine repairs, preventative maintenance schedules, downhole pump replacements. |

| Utilities | Energy costs required for operations. | Electricity to power artificial lift systems (pumpjacks, ESPs), fuel for compressors. |

| Fluid Management | Costs associated with handling all produced fluids, especially water. | Saltwater disposal (SWD) fees (per barrel), water hauling/trucking costs. |

| Chemicals | Chemicals used to treat fluids and protect equipment. | Corrosion inhibitors, paraffin solvents, H2S scavengers, scale inhibitors. |

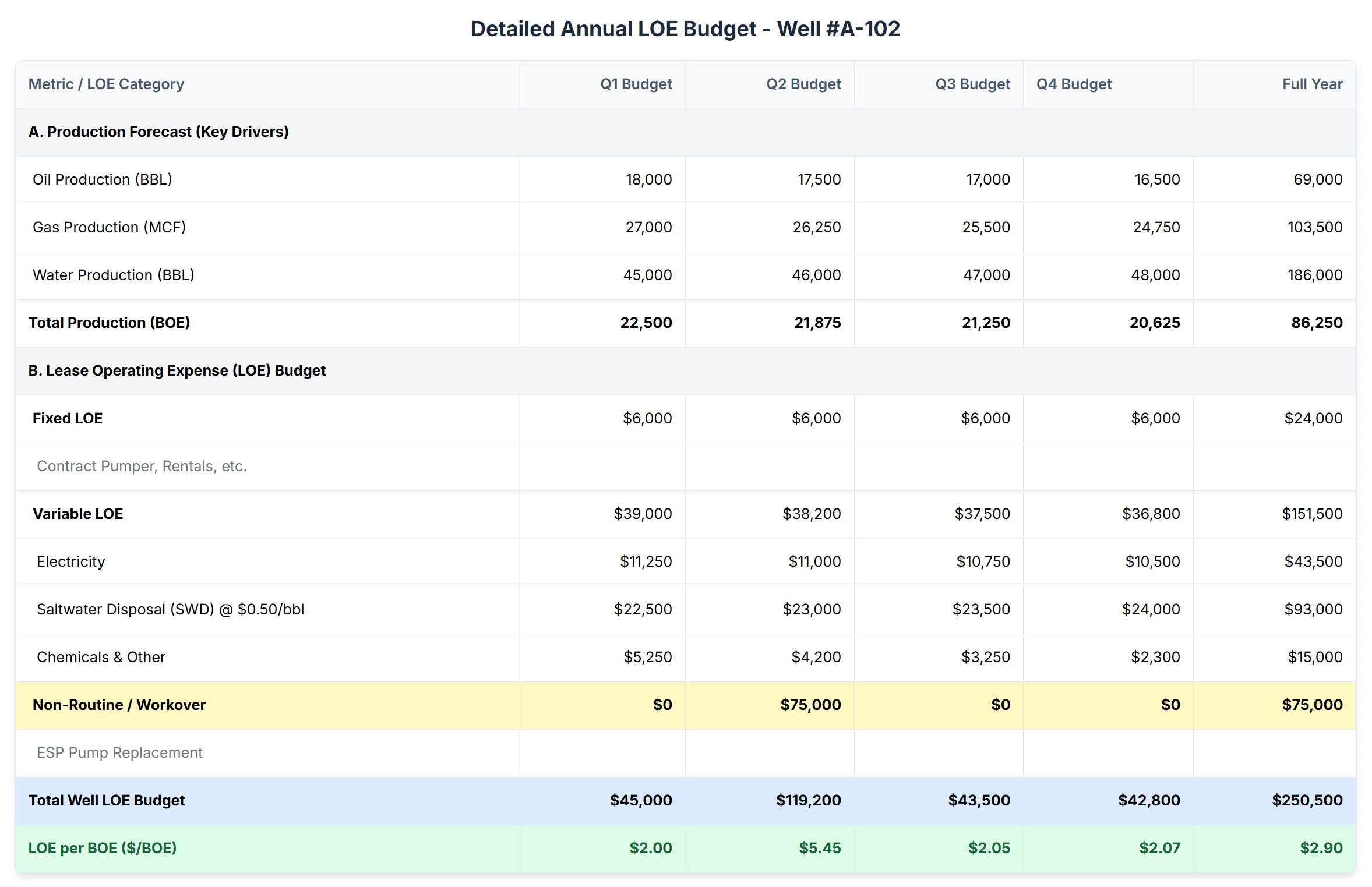

This is the most fundamental concept in LOE budgeting. To build an accurate and flexible plan, you must segregate your costs based on their behavior.

Fixed LOE costs are incurred regardless of how much oil, gas, or water a well produces. Think of them as the base operating cost for having the well active. This includes items like the monthly contract pumper fee, surface equipment rental fees, and basic site maintenance. They are predictable and stable.

Variable LOE costs, on the other hand, fluctuate directly with the volume of fluids moving through the system. As production changes, these costs change. This is especially true for water production, which is a major cost driver. The more fluid you lift, the more electricity you use. The more water you produce, the more you pay in saltwater disposal (SWD) fees. Chemical treatment costs also rise with higher fluid volumes.

Understanding this distinction is critical for accurate forecasting. If your production forecast is revised mid-year, you know your variable LOE will change with it, while your fixed LOE will remain largely the same. This is the key to creating a truly dynamic financial model.

Building a comprehensive LOE budget is a cross-functional exercise that requires tight collaboration between finance, engineering, and field operations.

An LOE budget is not a "set it and forget it" document. It's a living tool used to manage performance and drive operational efficiency throughout the year.

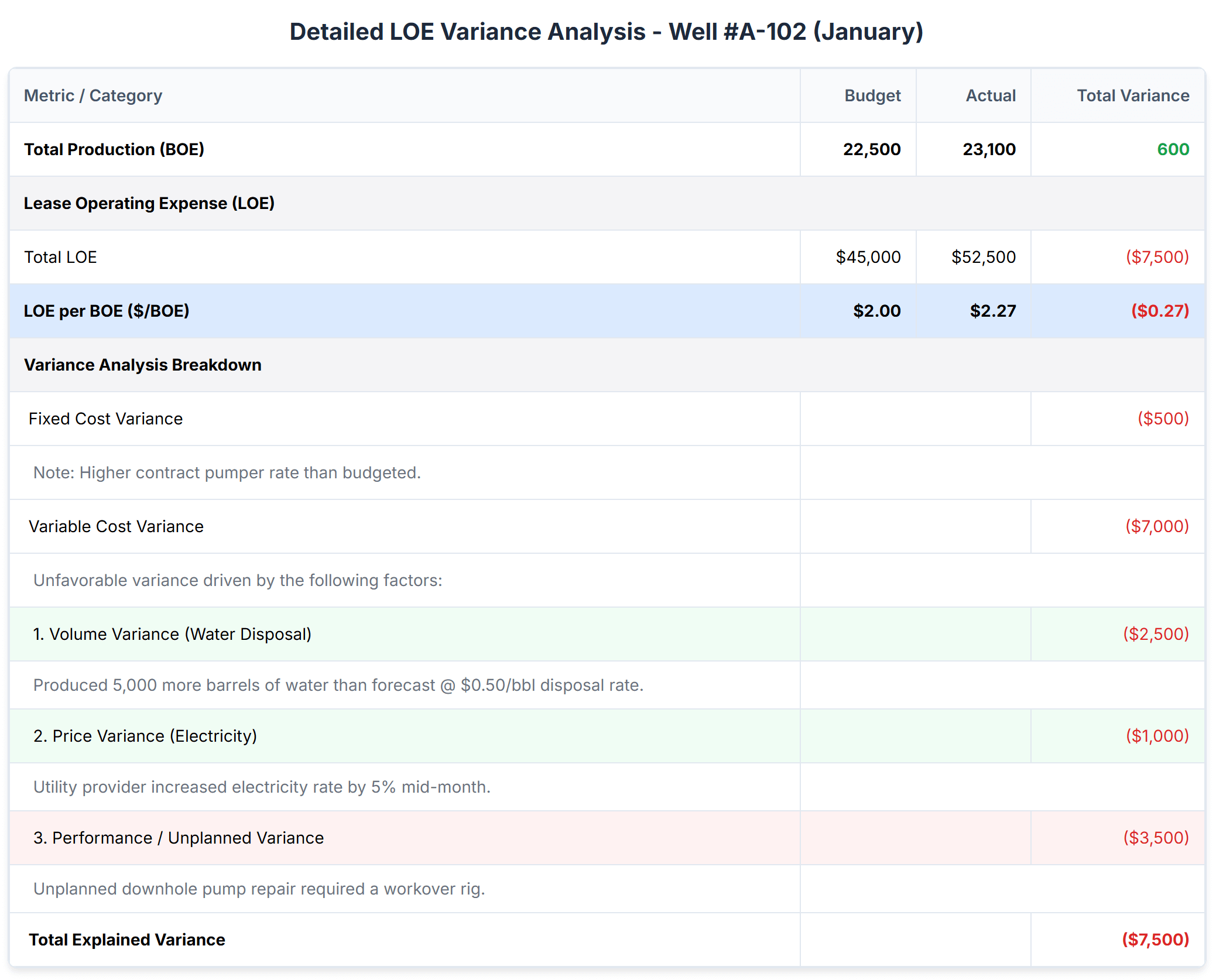

The primary mechanism for this is Monthly Variance Analysis. At the end of each month, the actual LOE is compared to the budget, and the goal is to understand the story behind any differences. Diagnosing the variance is key. Was an overspend caused by an unexpected equipment failure that required expensive repairs (a maintenance variance)? Or was it because the well produced more water than forecasted, leading to higher disposal fees (a volume variance)? Or perhaps the electricity provider raised their rates (a price variance)? Each diagnosis leads to a different action.

Ultimately, all of this analysis rolls up into the most important operational KPI: LOE per Barrel of Oil Equivalent (BOE). This metric is calculated as (Total LOE) / (Total Production in BOE). It normalizes costs and allows for a true "apples-to-apples" comparison of operational efficiency across different wells, fields, and even against competitors. It answers the fundamental question: "How efficiently are we producing each barrel?"

Disciplined LOE budgeting is a critical operational and financial function in the Oil & Gas industry. It requires a detailed understanding of fixed vs. variable cost structures, a tight collaboration with engineering and field operations, and a rigorous performance management loop.

Effective LOE management is not simply about cutting costs. It is a strategic lever that directly impacts the profitability and economic lifespan of every well in your portfolio. By mastering the LOE budget, a company transforms a major cost center into a key driver of asset value and a source of competitive advantage.

Lumel enables oil & gas teams to turn LOE data into actionable insight—streamlining budgets, tracking performance, and optimizing every barrel. With Lumel, LOE becomes not just a cost to manage, but a lever to unlock asset value. The firm was recognized as the Best Overall Vendor for EPM in 2025.

To follow our experts and receive thought leadership insights on data & analytics, register for one of our webinars. To learn how Lumel Enterprise Performance Management (EPM) supports new product introductions, reach out to us today.